Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Your Beginner’s Guide to Home Appraisals

Appraisals are used as a reliable, independent valuation of a tract of land and the structure on it, whether it’s a house or a skyscraper. Designed to protect buyers, sellers, and lending institutions, appraisals are an important part of the buying/selling process.

Below, you will find information about the appraisal process, what goes into them, their benefits and some tips on how to help make an appraisal go smoothly and efficiently.

Appraisal value vs. market value

The appraiser’s value is determined by using a combination of factors such as comparative market analyses and their inspection of the property to determine if the listing price is typical for the area.

Market value, on the other hand, is what a buyer is willing to pay for a home or what homes of comparable value are selling for.

If you are in the process of setting the price of your home, you can gain some peace-of-mind by consulting an independent appraiser. Show them comparative values for your neighborhood, relevant documents, and give them a tour of your home, just as you would show it to a prospective buyer.

What information goes into an appraisal?

Professional appraisers consult a range of information sources, including multiple listing services, county tax assessor records, county courthouse records, and appraisal data records, in addition to talking to local real estate professionals.

They also conduct an inspection. Typically, an appraiser’s inspection focuses on:

- The condition of the property and home, inside and out.

- The home’s layout and features.

- Home updates.

- Overall quality of construction.

- Estimate of the home’s square footage (the gross living area “GLA”; garages and unfinished basements are estimated separately).

- Permanent fixtures (for example, in-ground pools, as opposed to above-ground pools).

After the inspection, the appraiser of a typical single-family home will create their report including their professional opinion on what the price of the home should be.

You might hear the lender ask for two reports, the “Sales Comparison Approach” and the “Cost Approach.” These two approaches use different methodologies to find the appropriate value of the home, and help the lender confirm the home’s price.

Who pays and how long does it take?

The buyer usually pays for the appraisal unless they have negotiated otherwise. Depending on the lender, the appraisal may be paid in advance or incorporated into the application fee; some are due on delivery and some are billed at closing. Typical costs range from $275-$600, but this can vary from region to region.

An inspection usually takes anywhere from 15 minutes to several hours, depending on the size and complexity of your property. In addition, the appraiser spends time pulling up county records for the values of the houses around you. A full report is sent to your loan officer, real estate agent, and/or lender in about a week.

If you are the seller, you won’t get a copy of an appraisal ordered by a buyer. Under the Equal Credit Opportunity Act, however, the buyer has the right to get a copy of the appraisal if they request it. Typically, the requested appraisal is provided at closing.

What if the appraisal is too low?

A low appraisal can present a problem when there’s a large difference between what you’ve agreed to pay and the appraisal price.

Usually, the seller’s agents and the buyer’s agent will respond by looking for recent sold and pending listings of comparable homes. Sometimes this can influence the appraisal. If the final appraisal is well below what you have agreed to pay, you can re-negotiate the contract or cancel it.

Where do you find a qualified appraiser?

Your bank or lending institution will find and hire an appraiser; Federal regulatory guidelines do not allow borrowers to order and provide an appraisal to a bank for lending purposes. If you want an appraisal for your own personal reasons and not to secure a mortgage or buy a homeowner’s insurance policy, you can do the hiring yourself. You can contact your lending institution and they can recommend qualified appraisers and you can choose one yourself or you can call your local Windermere Real Estate agent and they can make a recommendation for you. Once you have the name of some appraisers you can verify their status on the Federal Appraisal Subcommittee website.

Tips for hassle-free appraisals:

To ensure the appraisal process is smooth and efficient, provide your appraiser with the information and documents he or she needs to get the job done. The documents you will need include:

- A brief explanation of why you’re getting an appraisal

- The date you’d like your appraisal to be completed

- A copy of your deed, survey, purchase agreement, or other papers that pertain to the property

- A sketch of the property with the property’s dimensions. These are usually available online from the county assessors.

- If you have a mortgage, provide the information about your lender, the year you got your mortgage, the amount, the type of mortgage (FHA, VA, etc.), your interest rate, and any additional financing you have.

- A copy of your current real estate tax bill, statement of special assessments, balance owing and on what (for example, sewer, water)

- Tell your appraiser if your property is listed for sale and if so, your asking price and listing agency.

- If it’s a multiple offer situation, provide the appraiser with the other offers to prove the demand for the home.

- Any personal property that is included in the sale, like appliances and other fixtures.

- If you’re selling an income-producing property, a breakdown of income and expenses for the last year or two and a copy of leases.

- A copy of the original house plans and specifications.

- A list of recent improvements and their costs.

- Any other information you feel may be relevant.

By doing your homework, compiling the information your appraiser needs, and providing it at the beginning of the process, you can minimize unnecessary delays.

You’ve Moved into Your New Home. Now What?

Congratulations on your new home! You made it through the arduous process that is buying a new home. Now it’s time to take on the task of moving in.

You did your research about the neighborhood and you feel like you know the home like the back of your hand. However, there are some things to do as you move in to protect your newest investment, and yourself, from the unknown variables in and around your home.

Change the locks garage door codes

Previous owners might have changed the locks, but they may not know who all has a key or a code to open your garage, especially neighbors who they trusted to watch their place while they were away. Changing the codes and locks on all the doors ensures that you have complete control over entry to your home

Check or Install Fire and Carbon Monoxide Detectors

If the home already has fire and carbon monoxide devices, make sure they are in working order by testing each one with the tester button. Keep a note of when to replace them as well.

If they don’t have them, install a device in each sleeping room, as well as common areas like the living room or kitchen. Hallways are a great place to cover multiple rooms with one detector as well.

Install a security system

Enjoy total peace of mind with a new security system. Meet with a consultant on the best ways to protect your home for a system that works best for you and your lifestyle.

There are also app-connected systems that you can set up yourself that notify you of movement on the cameras or doors and windows opening.

Meet the neighbors

Build a sense of community and get to know the lay of the land by knocking on neighbors’ doors to get to know them. Bring a small gift as a “thank you” for dealing with the moving trucks. This is a great initial step for figuring out who you can trust to watch things while you’re away should you need a helping hand in the near future.

The Impact of Staging Your Home

For more than 20 years, the benefits of staging a home have been well documented. Numerous studies show that staging helps sell a home faster and for a higher price. According to the National Association of REALTORS®, 88 percent of home buyers start their search online, forming impressions within three seconds of viewing a listing. When a home is well staged, it photographs well and makes the kind of the first impression that encourages buyers to take the next step.

Studies also indicate that buyers decide if they’re interested within the first 30 seconds of entering a home. Not only does home staging help to remove potential red flags that can turn buyers off, but it also helps them begin to imagine living there. Homes that are professionally staged look more “move-in ready” and that makes them far more appealing to potential buyers.

According to the Village Voice, staged homes sell in one-third less time than non-staged homes. Staged homes can also command higher prices than non-staged homes. Data compiled by the U.S. Department of Housing and Urban Development indicate that staged homes sell for approximately 17 percent more than non-staged homes.

A measurable difference in time and money

In a study conducted by the Real Estate Staging Association in 2007, a group of vacant homes that had remained unsold for an average of 131 days were taken off the market, staged, and relisted. The newly staged properties sold, on average, in just 42 days, – which is approximately 68 percent less time on the market.

The study was repeated in 2011, in a more challenging market, and the numbers were even more dramatic. Vacant homes that were previously on the market for an average of 156 days as unstaged properties, when listed again as staged properties, sold after an average of 42 days—an average of 73 percent less time on the market.

Small investments, big potential returns

Staging is a powerful advantage when selling your home, but that’s not the only reason to do it. Staging uncovers problems that need to be addressed, repairs that need to be made, and upgrades that should be undertaken. For a relatively small investment of time and money, you can reap big returns. Staged properties are more inviting, and that inspires the kind of peace-of-mind that gets buyers to sign on the dotted line. In the age of social media, a well-staged home is a home that stands out, gets shared, and sticks in people’s minds.

What’s more, the investment in staging can bring a higher price. According to the National Association of REALTORS, the average staging investment is between one percent and three percent of the home’s asking price, and typically generates a return of eight to ten percent.

In short, less time on the market and higher selling prices make the small cost of staging your home a wise investment.

Interested in learning more? Contact me for information about the value of staging and referrals for professional home stagers.

Windermere Living Fall Issue

Dear Readers,

Welcome to the fall issue of Windermere Living! Are you a foodie who loves to travel? Inside this issue is an article about interesting destinations where you can enjoy edible, immersive experiences like making your own coffee on the Kona coast of Hawaii, or diving for clams in Cabo and cooking them with an executive chef.

If you’ve ever undergone a major home remodel, you know all too well how important it is to partner with the right architect. We explore that topic in this issue, along with some pro tips on how to match yourself up with the perfect architect for your project, a process that isn’t that different from dating.

Last but not least, there are more than 70 pages filled with homes for sale throughout the Western U.S. Whether you’re in the market for a country farmhouse or a high-rise condo, there’s a little something for everyone.

This is just a sampling of what you’ll find in this issue of Windermere Living; we hope you enjoy it!

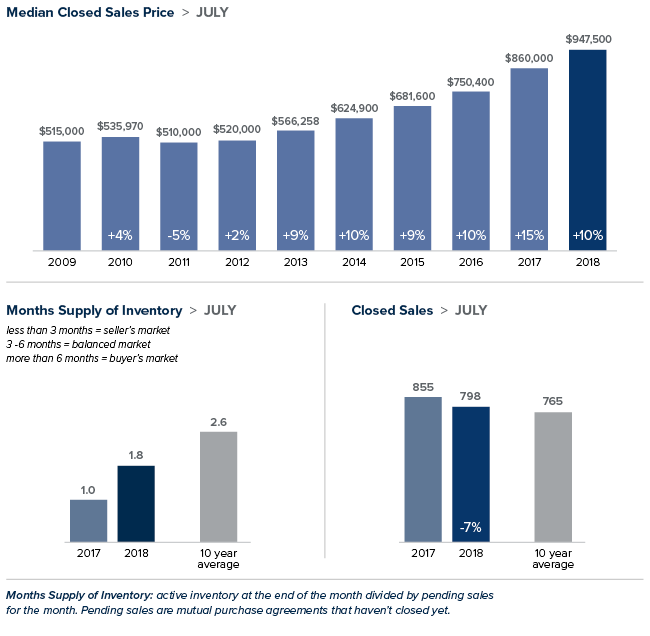

Local Market Update – August 2018

For the first time in years, the real estate market is finally starting to deliver good news for buyers. The region experienced its third straight month of significant growth in inventory. Homes are sitting on the market longer, prices are moderating, and multiple offers are becoming more rare. Despite the surge in homes for sale, it is still a seller’s market. Inventory would need to triple to reach what is considered a balanced market.

Eastside

Inventory on the Eastside soared 47 percent over the same time last year. There was a slight increase in new listings, but the jump was mostly due to homes staying on the market longer. Price drops have become more common. With buyers having more choices, sellers need to work with their broker to make sure they price their home correctly the first time. After setting a new high of $977,759 in June, the median price of a single-family home dropped to $947,500 in July. While offering some hope that prices may have started to moderate, the median is still 10 percent higher than it was the same time a year ago.

King County

King County saw the biggest increase in inventory in a decade, with the number of homes for sale jumping 48 percent over a year ago. However, at 1.5 months of supply that’s still well below the 4-6 months of inventory that is considered balanced. The median price of a single-family sold in July was $699,000. That represents an increase of 6 percent from a year ago, but is down 4 percent from the record high of $725,000 set in April. Perceptions that the market is cooling needs to be kept in perspective. Homes here took an average of 15 days to sell.

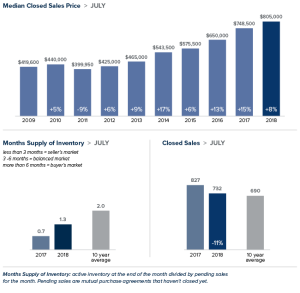

Seattle

Seattle saw inventory shoot up 60 percent over a year ago, bringing the supply to its highest level in over three years. Even with the sharp increase, much more inventory is needed to meet the demand for homes in the city and sellers may well decide to jump into the market. According to a Zillow study, more than 97 percent of homes in Seattle are worth more now than the peak level before the housing market crashed. Median home prices are 29 percent above the bubble peak level with the median price in July landing at $805,000; up 7 percent from last July and down from the record $830,000 reached in May.

Snohomish County

Snohomish County also had double-digit increases in inventory, though not nearly as great as King County. The number of homes for sale in July increased nearly 16 percent over the same time a year ago, but inventory continues to be very tight. The median price of a single-family home rose 9 percent year-to-year to $495,000. That figure is down from the record high of $511,500 set in June. A move towards a more moderated market is encouraging for buyers and an incentive for sellers to list their homes soon.

Windermere Teams Up with the Seahawks to #TackleHomelessness

Windermere is proud to partner with the Seattle Seahawks for the fourth season to help #TackleHomelessness. For every Seahawks home game defensive tackle, Windermere will donate $100 to Mary’s Place, whose mission is to help families on their journey out of homelessness. To date we’ve raised nearly $100,000 through our #TackleHomelessness campaign and we’re looking forward to raising even more for our friends at Mary’s Place!

The Slow Down in Foreign Buyers

The United States housing market is experiencing a significant reduction in foreign buyers. Windermere Chief Economist, Matthew Gardner, cites several factors that could be contributing to this trend and offers his opinions as to what to expect in this recent Market Update.

Western Washington Real Estate Market Update Q2

The following analysis of the Western Washington real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please contact me.

ECONOMIC OVERVIEW

Washington State employment jumped back up to an annual growth rate of 2.4% following a disappointing slowdown earlier in the spring. As stated in the first quarter Gardner Report, the dismal numbers earlier this year were a function of the state re-benchmarking its data (which they do annually).

The state unemployment rate was 4.7%, marginally up from 4.5% a year ago. My current economic forecast suggests that statewide job growth in 2019 will rise by 2.6%, with a total of 87,500 new jobs created.

HOME SALES

- There were 22,281 home sales during the second quarter of 2019, representing a drop of 4.8% from the same period in 2018. On a more positive note, sales jumped 67.6% compared to the first quarterof this year.

- Since the middle of last year, there has been a rapid rise in the number of homes for sale, which is likely the reason sales have slowed. More choice means buyers can be more selective and take their time when choosing a home to buy.

- Compared to the second quarter of 2018, there were fewer sales in all counties except Whatcom and Lewis. The greatest declines were in Clallam, San Juan, and Jefferson counties.

- Listings rose 19% compared to the second quarter of 2018, but there are still a number of very tight markets where inventory levels are lower than a year ago. Generally, these are the smaller — and more affordable — markets, which suggests that affordability remains an issue.

HOME PRICES

Year-over-year price growth in Western Washington continues to taper. The average home price during second quarter was $540,781, which is 2.8% higher than a year ago. When compared to first quarter of this year, prices were up 12%.

Year-over-year price growth in Western Washington continues to taper. The average home price during second quarter was $540,781, which is 2.8% higher than a year ago. When compared to first quarter of this year, prices were up 12%.- Home prices were higher in every county except King, which is unsurprising given the cost of homes in that area. Even though King County is home to the majority of jobs in the region, housing is out of reach for many and I anticipate that this will continue to act as a drag on price growth.

- When compared to the same period a year ago, price growth was strongest in Lewis County, where home prices were up 15.9%. Double-digit price increases were also seen in Mason, Cowlitz, Grays Harbor, and Skagit counties.

- The region’s economy remains robust, which should be a positive influence on price growth. That said, affordability issues are pervasive and will act as a headwind through the balance of the year, especially in those markets that are close to job centers. This will likely force some buyers to look further afield when searching for a new home.

Year-over-year price growth in Western Washington continues to taper. The average home price during second quarter was $540,781, which is 2.8% higher than a year ago. When compared to first quarter of this year, prices were up 12%.

Year-over-year price growth in Western Washington continues to taper. The average home price during second quarter was $540,781, which is 2.8% higher than a year ago. When compared to first quarter of this year, prices were up 12%. DAYS ON MARKET

DAYS ON MARKET

- The average number of days it took to sell a home matched the second quarter of 2018.

- Snohomish County was the tightest market in Western Washington, with homes taking an average of only 21 days to sell. There were five counties where the length of time it took to sell a home dropped compared to the same period a year ago. Market time rose in eight counties and two were unchanged.

- Across the entire region, it took an average of 41 days to sell a home in the second quarter of 2019. This was the same as a year ago but is down 20 days compared to the first quarter of 2019.

- As stated above, days-on-market dropped as we moved through the spring, but all markets are not equal. I suggest that this is not too much of an issue and that well-priced homes will continue to attract attention and sell fairly rapidly.

CONCLUSIONS

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors. I am leaving the needle in the same position as the first quarter as demand appears to still be strong.

The market has benefitted from a fairly significant drop in mortgage rates. With average 30-year fixed rates still below 4%, I expect buyers who have been sitting on the fence will become more active, especially given that they have more homes to choose from.

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

The Risks and Rewards of Purchasing a Bank-Owned Home

The process of purchasing a home directly from a lender can be long and arduous, but could very well be worth it in the end. If you have your sights on a particular home or are looking to find a deal on your first, working directly with the lender may be your only option. Purchasing a bank-owned home is not for the faint of heart, here are some tips for negotiating the REO process:

1. Be prepared: The condition of bank-owned properties are often poor and hard to show. Past owners may have departed on bad terms, leaving the home in poor condition with foul smells, missing appliances, wires are taken from breakers, gas fireplaces gone, even bathrooms without toilets and sinks.

2. Understand the costs: Maintenance or repairs may be necessary since these homes have been vacant for an unknown period of time–sometimes months or years. Keep in mind, when they were occupied the owners could have been under financial hardship, preventing them from doing regular seasonal care or repairs when needed. Remember as well that the bank is trying to sell the house immediately, so you will receive a financial break in the price rather than a willingness to negotiate on the maintenance and repair issues.

3. Accept the unknown: In traditional real estate transactions, homeowners fill out Form 17 regarding important information about the history of the house. A bank-owned home is either exempt or marked with “I don’t know” throughout the document. Not having the accuracy of this 5-page disclosure form could leave you with a lot of unanswered questions on the history of the home.

4. Know what is non-negotiable: The pricing on the house may not get much lower. Some of these properties can be “a dream come true” if you get them at an amazing price, or they could be your worst nightmare. Do your due diligence researching any property, and conduct all necessary inspections to safeguard yourself. Some major repairs may be negotiable, but will likely not reduce the home price.

5. Make a clean offer: The higher the price you can offer, the better. Include your earnest money, keep contingencies to a minimum, and suggest a reasonable closing date. The simpler your offer is, the higher chance you have of the bank accepting your offer or countering in a reasonable time period.

6. Be patient: Consult with a professional who handles bank owned home purchases to help you negotiate the pathway to homeownership. The process of purchasing a bank-owned, foreclosed or short-sale home is typically longer than a typical real estate sale.

Mortgage Rate Forecast

Geopolitical uncertainty is causing mortgage rates to drop. Windermere Chief Economist, Matthew Gardner, explains why this is and what you can expect to see mortgage rates do in the coming year.

Over the past few months we’ve seen a fairly significant drop in mortgage rates that has been essentially driven by geopolitical uncertainty – mainly caused by the trade war with China and ongoing discussions over tariffs with Mexico.

Now, mortgage rates are based on yields on 10-Year treasuries, and the interest rate on bonds tends to drop during times of economic uncertainty. When this occurs, mortgage rates also drop.

My current forecast model predicts that average 30-year mortgage rates will end 2019 at around 4.4%, and by the end of 2020 I expect to see the average 30-year rate just modestly higher at 4.6%.