Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Windermere Living Fall Issue

Dear Readers,

Welcome to the fall issue of Windermere Living! Are you a foodie who loves to travel? Inside this issue is an article about interesting destinations where you can enjoy edible, immersive experiences like making your own coffee on the Kona coast of Hawaii, or diving for clams in Cabo and cooking them with an executive chef.

If you’ve ever undergone a major home remodel, you know all too well how important it is to partner with the right architect. We explore that topic in this issue, along with some pro tips on how to match yourself up with the perfect architect for your project, a process that isn’t that different from dating.

Last but not least, there are more than 70 pages filled with homes for sale throughout the Western U.S. Whether you’re in the market for a country farmhouse or a high-rise condo, there’s a little something for everyone.

This is just a sampling of what you’ll find in this issue of Windermere Living; we hope you enjoy it!

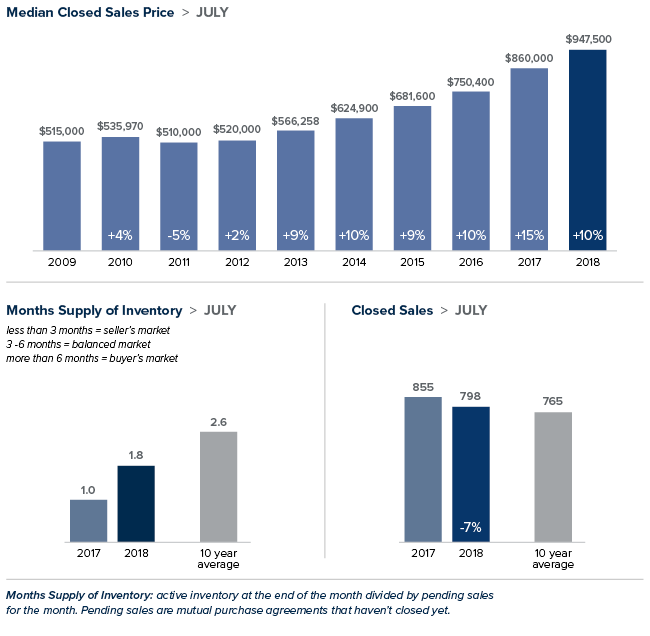

Local Market Update – August 2018

For the first time in years, the real estate market is finally starting to deliver good news for buyers. The region experienced its third straight month of significant growth in inventory. Homes are sitting on the market longer, prices are moderating, and multiple offers are becoming more rare. Despite the surge in homes for sale, it is still a seller’s market. Inventory would need to triple to reach what is considered a balanced market.

Eastside

Inventory on the Eastside soared 47 percent over the same time last year. There was a slight increase in new listings, but the jump was mostly due to homes staying on the market longer. Price drops have become more common. With buyers having more choices, sellers need to work with their broker to make sure they price their home correctly the first time. After setting a new high of $977,759 in June, the median price of a single-family home dropped to $947,500 in July. While offering some hope that prices may have started to moderate, the median is still 10 percent higher than it was the same time a year ago.

King County

King County saw the biggest increase in inventory in a decade, with the number of homes for sale jumping 48 percent over a year ago. However, at 1.5 months of supply that’s still well below the 4-6 months of inventory that is considered balanced. The median price of a single-family sold in July was $699,000. That represents an increase of 6 percent from a year ago, but is down 4 percent from the record high of $725,000 set in April. Perceptions that the market is cooling needs to be kept in perspective. Homes here took an average of 15 days to sell.

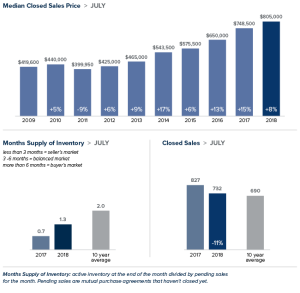

Seattle

Seattle saw inventory shoot up 60 percent over a year ago, bringing the supply to its highest level in over three years. Even with the sharp increase, much more inventory is needed to meet the demand for homes in the city and sellers may well decide to jump into the market. According to a Zillow study, more than 97 percent of homes in Seattle are worth more now than the peak level before the housing market crashed. Median home prices are 29 percent above the bubble peak level with the median price in July landing at $805,000; up 7 percent from last July and down from the record $830,000 reached in May.

Snohomish County

Snohomish County also had double-digit increases in inventory, though not nearly as great as King County. The number of homes for sale in July increased nearly 16 percent over the same time a year ago, but inventory continues to be very tight. The median price of a single-family home rose 9 percent year-to-year to $495,000. That figure is down from the record high of $511,500 set in June. A move towards a more moderated market is encouraging for buyers and an incentive for sellers to list their homes soon.

Windermere Teams Up with the Seahawks to #TackleHomelessness

Windermere is proud to partner with the Seattle Seahawks for the fourth season to help #TackleHomelessness. For every Seahawks home game defensive tackle, Windermere will donate $100 to Mary’s Place, whose mission is to help families on their journey out of homelessness. To date we’ve raised nearly $100,000 through our #TackleHomelessness campaign and we’re looking forward to raising even more for our friends at Mary’s Place!

The Slow Down in Foreign Buyers

The United States housing market is experiencing a significant reduction in foreign buyers. Windermere Chief Economist, Matthew Gardner, cites several factors that could be contributing to this trend and offers his opinions as to what to expect in this recent Market Update.

Western Washington Real Estate Market Update Q2

The following analysis of the Western Washington real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please contact me.

ECONOMIC OVERVIEW

Washington State employment jumped back up to an annual growth rate of 2.4% following a disappointing slowdown earlier in the spring. As stated in the first quarter Gardner Report, the dismal numbers earlier this year were a function of the state re-benchmarking its data (which they do annually).

The state unemployment rate was 4.7%, marginally up from 4.5% a year ago. My current economic forecast suggests that statewide job growth in 2019 will rise by 2.6%, with a total of 87,500 new jobs created.

HOME SALES

- There were 22,281 home sales during the second quarter of 2019, representing a drop of 4.8% from the same period in 2018. On a more positive note, sales jumped 67.6% compared to the first quarterof this year.

- Since the middle of last year, there has been a rapid rise in the number of homes for sale, which is likely the reason sales have slowed. More choice means buyers can be more selective and take their time when choosing a home to buy.

- Compared to the second quarter of 2018, there were fewer sales in all counties except Whatcom and Lewis. The greatest declines were in Clallam, San Juan, and Jefferson counties.

- Listings rose 19% compared to the second quarter of 2018, but there are still a number of very tight markets where inventory levels are lower than a year ago. Generally, these are the smaller — and more affordable — markets, which suggests that affordability remains an issue.

HOME PRICES

Year-over-year price growth in Western Washington continues to taper. The average home price during second quarter was $540,781, which is 2.8% higher than a year ago. When compared to first quarter of this year, prices were up 12%.

Year-over-year price growth in Western Washington continues to taper. The average home price during second quarter was $540,781, which is 2.8% higher than a year ago. When compared to first quarter of this year, prices were up 12%.- Home prices were higher in every county except King, which is unsurprising given the cost of homes in that area. Even though King County is home to the majority of jobs in the region, housing is out of reach for many and I anticipate that this will continue to act as a drag on price growth.

- When compared to the same period a year ago, price growth was strongest in Lewis County, where home prices were up 15.9%. Double-digit price increases were also seen in Mason, Cowlitz, Grays Harbor, and Skagit counties.

- The region’s economy remains robust, which should be a positive influence on price growth. That said, affordability issues are pervasive and will act as a headwind through the balance of the year, especially in those markets that are close to job centers. This will likely force some buyers to look further afield when searching for a new home.

Year-over-year price growth in Western Washington continues to taper. The average home price during second quarter was $540,781, which is 2.8% higher than a year ago. When compared to first quarter of this year, prices were up 12%.

Year-over-year price growth in Western Washington continues to taper. The average home price during second quarter was $540,781, which is 2.8% higher than a year ago. When compared to first quarter of this year, prices were up 12%. DAYS ON MARKET

DAYS ON MARKET

- The average number of days it took to sell a home matched the second quarter of 2018.

- Snohomish County was the tightest market in Western Washington, with homes taking an average of only 21 days to sell. There were five counties where the length of time it took to sell a home dropped compared to the same period a year ago. Market time rose in eight counties and two were unchanged.

- Across the entire region, it took an average of 41 days to sell a home in the second quarter of 2019. This was the same as a year ago but is down 20 days compared to the first quarter of 2019.

- As stated above, days-on-market dropped as we moved through the spring, but all markets are not equal. I suggest that this is not too much of an issue and that well-priced homes will continue to attract attention and sell fairly rapidly.

CONCLUSIONS

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors. I am leaving the needle in the same position as the first quarter as demand appears to still be strong.

The market has benefitted from a fairly significant drop in mortgage rates. With average 30-year fixed rates still below 4%, I expect buyers who have been sitting on the fence will become more active, especially given that they have more homes to choose from.

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

The Risks and Rewards of Purchasing a Bank-Owned Home

The process of purchasing a home directly from a lender can be long and arduous, but could very well be worth it in the end. If you have your sights on a particular home or are looking to find a deal on your first, working directly with the lender may be your only option. Purchasing a bank-owned home is not for the faint of heart, here are some tips for negotiating the REO process:

1. Be prepared: The condition of bank-owned properties are often poor and hard to show. Past owners may have departed on bad terms, leaving the home in poor condition with foul smells, missing appliances, wires are taken from breakers, gas fireplaces gone, even bathrooms without toilets and sinks.

2. Understand the costs: Maintenance or repairs may be necessary since these homes have been vacant for an unknown period of time–sometimes months or years. Keep in mind, when they were occupied the owners could have been under financial hardship, preventing them from doing regular seasonal care or repairs when needed. Remember as well that the bank is trying to sell the house immediately, so you will receive a financial break in the price rather than a willingness to negotiate on the maintenance and repair issues.

3. Accept the unknown: In traditional real estate transactions, homeowners fill out Form 17 regarding important information about the history of the house. A bank-owned home is either exempt or marked with “I don’t know” throughout the document. Not having the accuracy of this 5-page disclosure form could leave you with a lot of unanswered questions on the history of the home.

4. Know what is non-negotiable: The pricing on the house may not get much lower. Some of these properties can be “a dream come true” if you get them at an amazing price, or they could be your worst nightmare. Do your due diligence researching any property, and conduct all necessary inspections to safeguard yourself. Some major repairs may be negotiable, but will likely not reduce the home price.

5. Make a clean offer: The higher the price you can offer, the better. Include your earnest money, keep contingencies to a minimum, and suggest a reasonable closing date. The simpler your offer is, the higher chance you have of the bank accepting your offer or countering in a reasonable time period.

6. Be patient: Consult with a professional who handles bank owned home purchases to help you negotiate the pathway to homeownership. The process of purchasing a bank-owned, foreclosed or short-sale home is typically longer than a typical real estate sale.

Mortgage Rate Forecast

Geopolitical uncertainty is causing mortgage rates to drop. Windermere Chief Economist, Matthew Gardner, explains why this is and what you can expect to see mortgage rates do in the coming year.

Over the past few months we’ve seen a fairly significant drop in mortgage rates that has been essentially driven by geopolitical uncertainty – mainly caused by the trade war with China and ongoing discussions over tariffs with Mexico.

Now, mortgage rates are based on yields on 10-Year treasuries, and the interest rate on bonds tends to drop during times of economic uncertainty. When this occurs, mortgage rates also drop.

My current forecast model predicts that average 30-year mortgage rates will end 2019 at around 4.4%, and by the end of 2020 I expect to see the average 30-year rate just modestly higher at 4.6%.

Five Things to Consider When Downsizing

Downsizing is on the minds of many homeowners today. Some are ready to retire, others want to live more simply, and many want to save money and say goodbye to home maintenance. If you can relate to any of those sentiments, ask yourself these five questions:

Have you done the math?

The financial savings that can be generated by downsizing can be significant – especially as they add up over time. When doing the math, make sure the move will save money, rather than spend unnecessarily.

Have you researched elder-care options?

Many homeowners hold on to their current home longer than they should because their parents / parents-in-law may need to come live with them in the future. While a noble gesture, there are many excellent elder care living options available today. Often, all it takes is a tour of those facilities to realize that your loved one may actually be happier, and far better served, in a place devoted to their care and happiness.

Have you considered off-site storage?

You don’t need to immediately discard a big chunk of your belongings in order to downsize. In fact, trying to do so in one fell swoop only creates needless stress. Most people find it works much better to move some of their belongings into off-site storage for six months. During that time, you can gradually incorporate some of those items into your new living arrangement, and slowly figure out what to do with the others.

How do you feel about sharing costs and decision-making?

Townhomes and condominiums are popular downsizing options. But both require that you share the decision-making and expenses associated with any maintenance and improvement projects with your neighbors and potentially an HOA. If you’re a people-person and agree that two heads are better than one, and you like the idea of sharing the cost/responsibility for expensive repairs, you’ll enjoy condo living. If not, this may not be the best option for you.

Have you consulted with a real estate agent?

Many homeowners don’t think to consult with a real estate agent until they’ve made the decision to downsize. This leads to guesstimating about some of the most important factors. The truth is, your real estate agent is someone you want to talk with very early in the decision-making process.

Improve Your Curb Appeal with These Affordable Tips

You’ll never have a second chance at a first impression, so let’s make it count! When it comes to upping your home’s curb appeal, there are plenty of small changes you can make that have a big impact. And best of all, you don’t need to call in the pros or spend a fortune to get beautiful results. Below are some helpful and affordable tips.

A Well-Maintained Yard

Mowing: The first step to a well-manicured lawn is to mow it regularly. The experts recommending mowing high because mowing it too short can damage the grass and allow weeds to set root.

Weeds: To prevent weeds like crabgrass use a pre-emergent herbicide in early spring. These herbicides manage the weeds by stopping the seeds from sprouting in your lawn. Broadleaf weeds like dandelions can be stopped by applying granular weed control products.

Feeding: Lawns consume mostly nitrogen, so look for mixes of fast and slow release fertilizers; they will feed your lawn over time while keeping it lush and green.

Watering: Nighttime watering can result in long spans of moisture on the blades, potentially exposing your grass to disease. Consider watering your lawn in the morning – the sun helps dry out the blades throughout the day.

Flowers: You can quickly and affordably dress up your yard with colorful pre-made flower pots and containers. When placing your flower pots and containers remember that asymmetrical arrangements and staggering plants will provided the liveliest setting.

Dress up the Front Door and Porch

Paint: A fresh coat of paint in a pop color can give your home a well-deserved facelift. Get some color inspiration from House Beautiful.

Replace Old Hardware: Clean off any dirty spots around the door knob, and use a metal polish on the fixtures. Change out house numbers for an updated feel, put up a wall-mounted mailbox, or add an overhead light fixture. Keep in mind that well thought through elements, instead of mix-and-match pieces, will add the most curb appeal.

Create Perfect Symmetry: Symmetry is one of the simplest design techniques to master and is the most pleasing to the eye. Maintain symmetry by flanking your front door with two sidelights (just make sure that your hardware matches); find two urn planters or a unique visual detail to put on either side of your door.

Renting vs Buying: Which is better for you?

The debate about whether it makes more financial sense to rent or buy has been raging for decades. Advocates of buying argue that when you pay rent you’re paying for someone else’s mortgage. When you buy, you are making an investment, which can significantly increase in value every year you live in the home.

Supporters of renting say that the extra costs associated with owning a home, such as interest payments, taxes, maintenance, can add up. They add that there’s no guarantee that those expenses will be recouped when the house is sold. Instead of investing in a home, you may be better off investing your savings in stocks, bonds, and other financial securities that hold less risk.

Matthew Gardner, our Chief Economist, forecasts, that we will not break 5% for 30-year fixed Mortgage rates for 2019, and likely won’t break it next year.

This means that getting a mortgage is relatively cheap, raising the question, ‘Is it really worth it to keep renting?’

Even if interest rates stay low, whether to rent or buy has a lot to do with each person’s specific situation. Here are a few considerations to make as you decide.

What’s the real estate situation in your city?

Industry groups put out reports every quarter stating the average national sales price for a home, and the average monthly payment for a U.S. rental. These reports are typically based on an average of all the cities in the U.S. But what really matters is what the numbers show when you dig into them on a local level.

Investigate the local sales and rental markets, and you’ll see there are some cities that fall well below that average, and some that rise far above it. When comparing housing costs, be sure to base your evaluation on what’s happening in your city and neighborhood, not the nationwide averages.

How long do you expect to live there?

If you don’t plan to be living in the same place for at least five years, renting is probably your best bet financially. But if you think you’re ready to settle down for as long as 7 to 10 years, chances are very good that any home you purchase will appreciate during that time even if the economy runs into some bumps along the way.

What’s the mortgage rate?

One of the other key factors to consider is the cost of your loan (the interest you’ll pay the lender). Fortunately, our Chief Economist, Matthew Gardner, does not expect interest rates to hit or break 5 percent, meaning money is relatively cheap.

Your mortgage rate will depend on how much money you have saved, your credit score, and other factors, so make sure to talk to a loan officer before you start looking for a home. Being pre-approved for a mortgage narrows down your price range and helps strengthen your offer when it comes time to compete for your new home.

Can you pay a bit more?

It can be advantageous to work a lower monthly payment to the bank so that you can pay a little more than the payment.

For example, if you can afford to pay a little extra towards your mortgage bill each month, say $300 more per month, on a 30-year, $300,000 loan, can knock eight years off the life of the loan and reduce your final bill by more than $63,000. That’s savings you would never see if you rented.

Will you need to make repairs or improvements?

Buying a fixer-upper may seem like a great way to get a deal on a house, but if the money you spend on the repairs is too great, your profit could be diminished when it comes time to sell. The same is true for remodeling and improvement projects.

Additionally, you can work with your Mortgage lender for a repair loan. This can help you get that lot you want, and help you pay for the repairs.

But ultimately, if you can only afford a home that demands major improvements, and you don’t have the skills to do much of the work yourself, it’s probably better to rent.

Do you have other ways to invest?

Many see a home purchase as an easy way to invest—a place where they can generate savings through home equity. But others say you can make more money renting an apartment and investing your savings in stocks, bonds, and other financial securities.

This is where a financial advisor might come in. They’ll be able to break down what you need to do in order to get the best return on your investments. They’ll also be able to see the big picture when it comes to your money.

Can you rent part of the house?

Speaking of a diverse portfolio, let your investment work for you. If you buy a house that includes a rental (extra bedroom, mother-in-law unit, etc.), you could be the landlord instead of paying the landlord. With that rental income, you could pay off the mortgage faster and contribute more to your savings. But, of course, you need to be willing to share your home with a tenant and take on the responsibilities of being a landlord or working with a professional property manager to help you with those duties.

Making your decision

To make your decision about whether to rent or buy easier, input the key financial facts regarding your situation into this Realtor.com Rent vs. Buy Calculator: For help making sense of the results and analyzing other factors, contact me.